How lending is the new way of investing?

03 Dec 2019Lorem Ipsum is simply dummy text of the printing and typesetting industry. Lorem Ipsum has been the industry's standard dummy text ever since the 1500s

P2P lending is fast catching on in India as an alternative investment avenue. At a time when equity is volatile, bond yields are falling and realty is no longer the sure-shot bet; p2p lending is surely emerging as one way of making alternative investments with improved tools of risk management. Here is why it makes sense to lenders.

One of the basic rules of the financial markets has been that regulated growth is always preferred over unregulated growth. RBI has set some clear regulations pertaining to capital adequacy of p2p lenders, loan limits that can be disbursed, exposure limits to a single borrower, and bar on cash transactions. This will ensure that the growth of p2p lending is orderly and gradual and the interests of the p2p lenders are protected. It also gives the lenders on the p2p platform greater comfort.

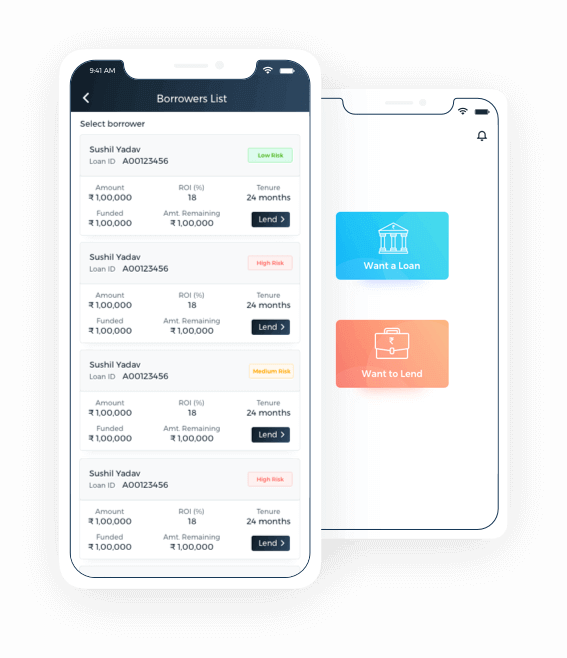

P2P lending platforms typically grade registered borrowers on their credit score and credit risk assessment. Low risk borrowers can get loans at around 14-15% while the high risk borrowers can get loans at closer to 27-30%. Overall, the average yield for the p2p lender works out closer to the range of 23-25%. That is the kind of returns that investors cannot expect today on any other investment. P2P lending helps enhance yields.

P2P lending diversifies risk for the lender in 3 ways. Firstly, this business is not cyclical and hence does not move in tandem with other asset classes like equities, bonds or even gold. Secondly, the limit of Rs.50,000 per borrower from one lender compels the P2P lender to spread the lending portfolio across multiple borrowers. This automatically diversifies risk. Lastly, the p2p lending platform uses technology to classify borrowers as high risk, medium risk and low risk. This allows p2p lenders to spread their money across risk classes too.

2P lending is a technology driven platform and relies largely on credit assessment and risk profiling. The platform uses the CIBIL score as a starting point and then combines factual and psychological parameters to arrive at a risk assessment of the borrower. This gives a very transparent view of the borrower and the lender can assess the risk based on the voluminous information on the borrower that is made available.

Above all, P2P lending is simple and cost effective. It is simple in terms of on-boarding the p2p lending platform. The loan documentation is entirely online and hence the costs are very low. That is all possible only because these platforms rely heavily on the use of technology to execute loan deals.

P2P lending combines returns, simplicity and risk management to offer unique alternative investment products to lenders.